Subscribe

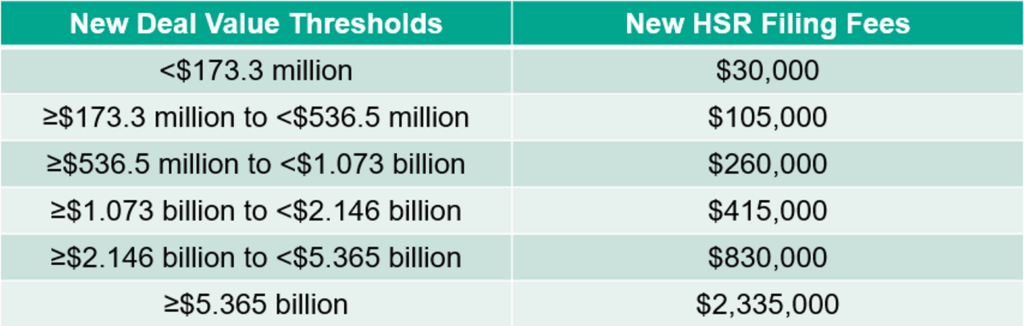

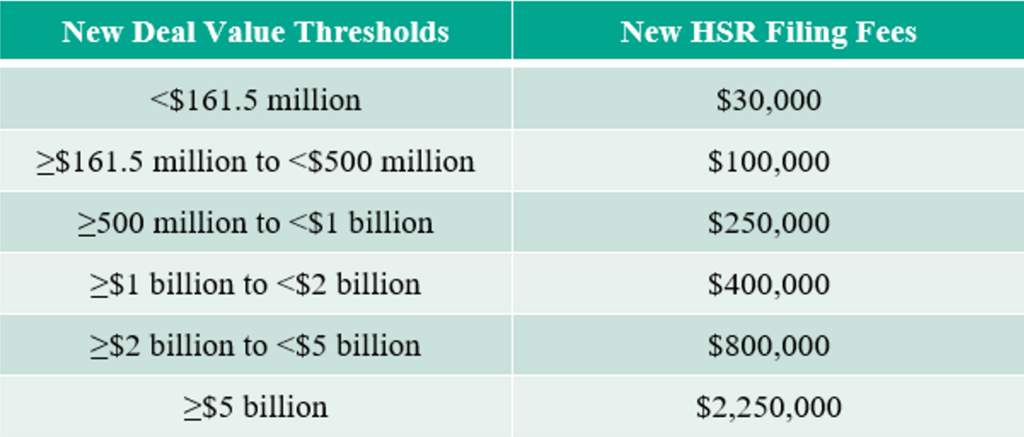

SubscribeOn January 14, 2026, the Federal Trade Commission (FTC) released increased jurisdictional thresholds, filing fee thresholds, and filing fee amounts for merger notifications made pursuant to the Hart-Scott-Rodino Antitrust Improvements Act of 1976 (HSR Act). The FTC also revised thresholds for interlocking directorates under Section 8 of the Clayton Act.

read more